The first quarter of 2026 has come to a close, and the data analysts at the International Data Corporation (IDC) have unveiled their latest findings on global computing trends. Here at Digital Tech Explorer, we’ve been tracking the ongoing global memory crisis closely, and the results are a fascinating mix of resilience and caution. While the industry saw a modest 2.5% uptick in hardware volume during Q1, a shadow looms over the forecast for the remainder of the year.

A Tale of Two Markets: Regional Performance Disparities

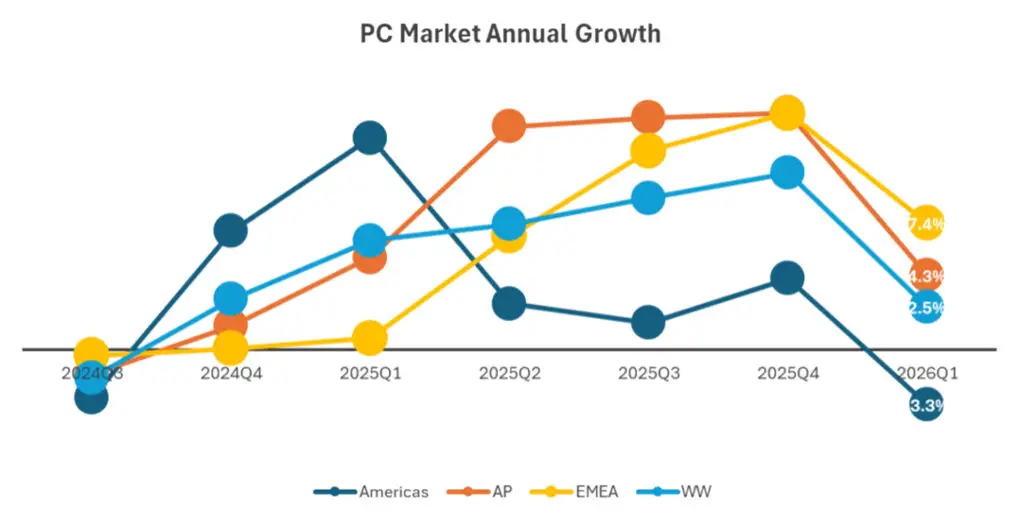

That 2.5% growth figure tells an incomplete story when viewed as a global average. When we dive into the specifics across the Americas, Asia Pacific, and EMEA (Europe, the Middle East, and Africa), the narrative shifts. The Asia Pacific region surged with a robust 4.3% growth, while EMEA outpaced everyone with an impressive 7.4% increase in unit deliveries.

The IDC data visualizes the stark contrast between emerging growth in EMEA and the struggles in the Western hemisphere.

Contrastingly, the Americas failed to join the celebration, experiencing a 3.3% decline. IDC suggests that while global momentum was fueled by the anticipation of rising component prices and the final stages of Windows 10 migration, the Americas likely plateaued due to high retail price tags. For the everyday tech enthusiast, this means the cost of entry for new hardware remains a significant barrier.

The Heavyweights: Top PC Vendors in Q1 2026

The leaderboard for top manufacturers remains relatively stable, though the volume gap between the “Big Three” and the rest of the pack is widening. Lenovo continues to dominate the landscape, leveraging its vast supply chain to navigate the current memory volatility.

Rank

Vendor

Units Shipped (Millions)

1

Lenovo

16.5

2

HP

12.1

3

Dell

10.3

4

Apple

6.2

5

Asus

4.8

Market share distribution among leading PC manufacturers for Q1 2026.

The HP Omen 35L. HP secured the second spot by focusing on high-performance machines for gaming and professional workloads.

Omdia’s Perspective: A Peak Before the Valley?

Validating the IDC report, research firm Omdia observed a similar 3.2% growth during the same period. However, their analysis carries a more urgent warning. Ben Yeh, Principal Analyst at Omdia, notes that Q1 likely represents the “high-water mark” for 2026.

The looming threat isn’t just demand; it’s the cost of production. Omdia predicts that memory and storage expenses will climb even more steeply starting in Q2. As a result, vendors may be forced to choose between shrinking their profit margins or passing those costs directly to you, the consumer. For those looking to build new gaming setups, this signals a period of “wait and see” or strategic buying.

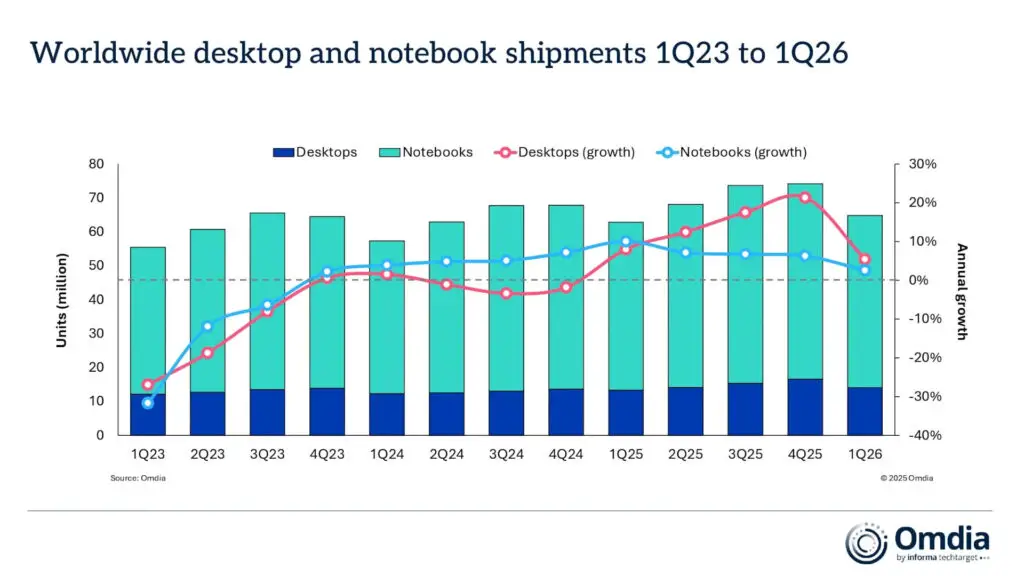

Omdia’s composite data highlights the volatility in laptop vs. desktop shipments as supply chain pressures mount.

Navigating the Storm: TechTalesLeo’s Final Word

As we navigate these shifting digital tides, the message for our community at Digital Tech Explorer is clear: maintain what you have. With logistical spikes and energy costs straining global freight, the price of a high-end GPU or a complete pre-built rig is unlikely to drop anytime soon.

Isaac Ngatia of IDC highlighted that geopolitical conflicts have injected a fresh layer of volatility into an already fragile market. This isn’t just about spreadsheets and shipment numbers; it’s about the everyday usability of technology. Whether you are a developer optimizing code or a enthusiast chasing 4K resolution, the road through 2026 requires careful investment and a focus on longevity.

Stay tuned to Digital Tech Explorer as we continue to track these trends and provide you with the insights needed to stay ahead in an ever-evolving tech landscape.